Factoring and Receivables Finance

What is Factoring?

Like the transfer of commercial paper, the transfer of receivables allows a company to obtain cash very quickly. This transfer takes place within the framework of a financial technique, called factoring.

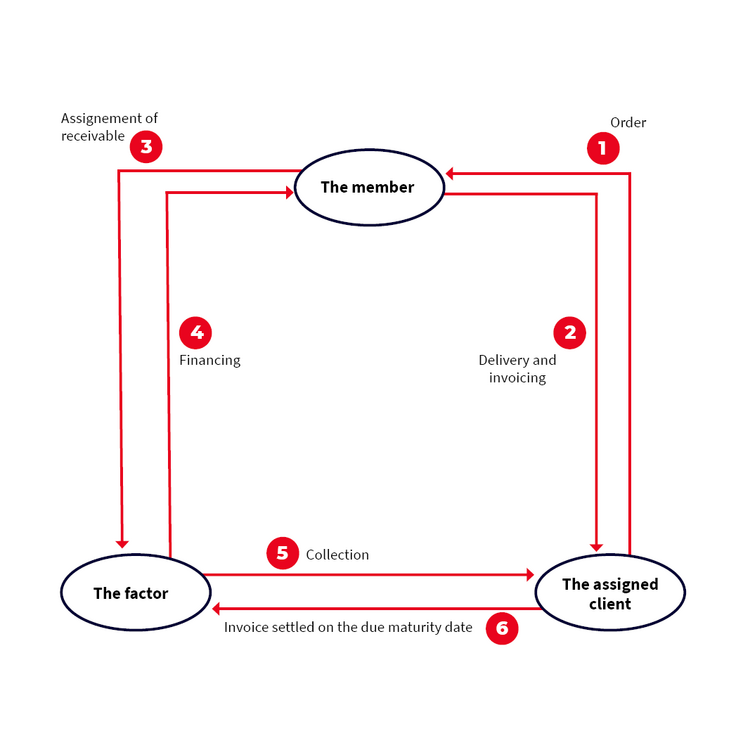

Factoring is a financing technique allowing a company (the member) to transfer its receivables from a customer (the assigned customer) to a financial institution specialized in factoring (called the factor).

Even if it can be a punctual financing via the session of some receivables, it is rather a financing in time. Indeed the contracts can go up to 5 years. The factor must therefore decide:

- The type of receivables he is ready to buy (average amount, duration);

- The assigned customers on which it is willing to take a risk.

The cost of Factoring is composed of a factoring commission and a financing commission.

- The financing commission corresponds globally to the interest rates since it is primarily a cash advance;

- The factoring commission corresponds to the cost of collecting the receivables (cost of managing the file, reminders, losses, etc.)

What are the advantages of Factoring for the member?

- The member is credited quickly (24 to 48 hours depending on the factor) and has a greater visibility on his cash flow and optimizes it.

- This technique can also be used to meet an occasional cash flow need.

- Factoring is useful to support a company in a growth phase.