Une nouvelle ere pour la transition ecologique en Asie

Les experts des Activités de Marchés Société Générale partagent leurs points de vue sur les moteurs et les stratégies qui façonnent la transition écologique en Asie, et sur ce que cela signifie pour les investisseurs.

Pour la première fois en février 2024, les températures moyennes mondiales enregistrées sur une période de 12 mois ont dépassé le seuil de 1,5°C au-dessus des niveaux préindustriels. Un seuil considéré comme critique par l'Accord de Paris de 2015.

L'Asie-Pacifique, qui représente plus de la moitié des émissions mondiales de CO2 et héberge trois des cinq principaux émetteurs de CO2 au monde, est au centre des efforts visant à réduire les émissions de carbone.

Abritant environ 60 % de la population mondiale avec une espérance de vie moyenne de 74 ans , l'Asie devrait voir sa demande énergétique multipliée par 2,5 d'ici 2050, sous l’effet du développement économique, de la croissance démographique et de l’urbanisation . La transition écologique représente à la fois d'énormes défis et de vastes opportunités pour cette région.

Différentes voies vers la neutralité carbone

Wei Yao, Cheffe Economiste et Responsable de la Recherche Asie-Pacifique, souligne que les gouvernements encouragent généralement la décarbonation en augmentant le coût du carbone pour rendre les émissions plus onéreuses, et/ou en abaissant le coût des alternatives à faible émission de carbone pour stimuler la demande. L'Europe a tendance à privilégier la première solution, tandis qu'en Asie, les choix sont contrastés. La Chine penche nettement vers la deuxième solution.

"Il s'agit d'une politique de lutte contre le changement climatique axée sur l'offre. L'approche est la suivante : nous construisons, et la demande viendra ensuite », dit-elle.

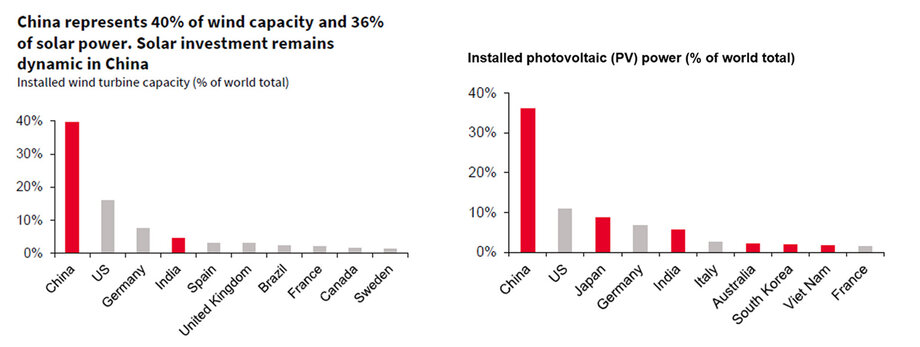

Les politiques de transition énergétique de la Chine ont permis de réduire le coût des technologies vertes, telles que l’énergie solaire. La Chine domine les chaînes d'approvisionnement des énergies renouvelables à l'échelle mondiale et est en bonne voie pour atteindre son objectif de 1200 gigawatts (GW) de capacité éolienne et solaire installée d'ici 2025, soit cinq ans plus tôt que prévu, selon une étude Société Générale.

Source : SG Cross Asset Research/Stratégie actions

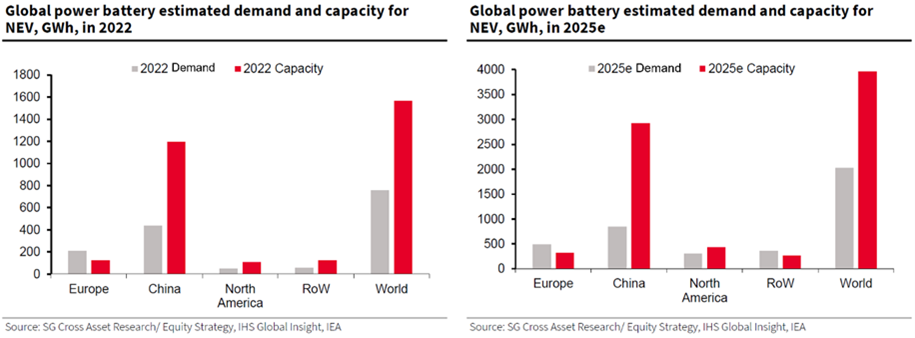

Ces politiques de l'offre risquent toutefois de créer d'autres problèmes, tels que la surcapacité. Prenez l’exemple de la mobilité verte, où la Chine domine également : l’étude Société Générale prévoit que la demande mondiale de batteries pour véhicules électriques atteindra 2030 gigawattheures (GWh) d'ici 2025, tandis que la capacité de production atteindra 3970 GWh. En Chine, la capacité de production pourrait être jusqu'à 3,5 fois supérieure à la demande intérieure.

D'un autre côté, le Japon a misé sur l'innovation technologique pour décarboner son secteur de l'électricité. Il dépend encore des combustibles fossiles pour plus de 70 % de son approvisionnement en électricité, responsable d'environ la moitié des émissions de CO2 du pays. Outre les énergies renouvelables, la stratégie nationale se concentre sur des technologies telles que l'hydrogène, l'ammoniac, le nucléaire et le CCUS (captage, utilisation et stockage du carbone).

Dans toute la région Asie-Pacifique, le secteur de l'énergie propre est en constante évolution à mesure que les technologies sont améliorées et que la transition mondiale progresse. Pour compliquer encore les choses, les conflits géopolitiques et la dynamique commerciale remodèlent les chaînes de valeur soutenant la transition écologique de l'Asie, alors que les gouvernements, en particulier en Occident, cherchent à réduire leur dépendance à l’égard des matières premières et des composants importés, à encourager le recyclage et à s’orienter vers la production locale et la relocalisation à proximité.

« Comme nous le voyons à travers les différentes économies en Asie, il existe de nombreuses façons d'atteindre la neutralité carbone, et pas seulement une « seule bonne façon », explique Yao.

À la recherche d'opportunités pour la transition

Après que les thématiques d’énergies propres aient résisté à des vents contraires en 2023, dus à la combinaison de l'inflation élevée et de la hausse des taux d'intérêt, la question est de savoir s’il s’agit toujours de bons investissements en 2024.

Selon Frank Benzimra, Responsable Asie Equity Strategy and Multi-Asset Strategist « La bonne nouvelle, c’est que les valorisations ont chuté plus que les revenus, ce qui supprime la prime importante sur les actions liée à la transition écologique. Le secteur continue de bénéficier d'un fort soutien politique, et un environnement de taux plus favorable pourrait profiter au cycle d'investissement de croissance en 2024 ».

Les études sur le climat, telles que Climate Value-at-Risk, peuvent être appliquées pour aider les investisseurs à réduire leur exposition aux entreprises présentant un risque de transition plus élevé ou à identifier celles présentant un risque de transition plus faible.

Le passage des activités carbonées aux activités « vertes » attire de plus en plus l'attention des investisseurs institutionnels, en particulier ceux qui sont présents en Asie. Le marché des obligations de transition, bien qu'encore naissant et sans définition standardisée, connaît une croissance rapide et attire les investisseurs internationaux.

Le Japon, par exemple, est devenu la plus grande source d'émission d'obligations de transition et a établi la norme en introduisant l'une des premières taxonomies de transition au monde. Le gouvernement s'est récemment engagé à réaliser 150 000 milliards de yens (1 000 milliards de dollars) d'investissements public-privé sur 10 ans, dont 20 000 milliards de yens seront financés par des obligations souveraines de transition. La première adjudication d'obligations souveraines de transition a eu lieu le 14 février 2024 .

L’environnement, les chiffres et la confiance des tiers sont des facteurs clés pour les investisseurs lorsqu'ils évaluent si les objectifs de transition sont suffisamment ambitieux et si les antécédents sont solides.

La transition écologique en Asie est un sujet complexe, avec des pays qui évoluent dans différentes directions. Malgré les défis géopolitiques et les progrès technologiques rapides, la transition vers l’écologie présente de vastes opportunités et continuera d'être un thème prometteur pour les investisseurs.

1. https://www.ft.com/content/8927424e-2828-4414-86b7-f3a991214288

2. IEA, CO2 emissions from fuel combustion, global ranking, 2021; BP Statistical Review (2022), Carbon dioxide emissions from energy, 2021 share

3. 2020 data, United Nations World Population Prospects 2022

4. https://www.mas.gov.sg/news/speeches/2023/developing-the-ecosystem-for-energy-transition

5. Based on data from Bloomberg, as of 16 Jan 2024.

6. https://www.mof.go.jp/english/policy/jgbs/topics/press_release/20231207-001e.htm

À mesure que le conflit avec l’Iran s’enlise, de simples déclarations pourraient ne plus suffire à contenir la hausse...

Par Mark Chng, Responsable des ventes Fixed Income & Currencies pour l’Asie du Sud-Est, Société Générale

Par David Jiang, Responsable du Groupe Industrie, Industrie et Technologie, Asie-Pacifique.

Entretien avec Jeff Mortara, Co-Responsable mondial des marchés de capitaux actions (ECM), et Responsable Investment...

Nous sommes ravis de participer à Sibos 2026, le principal événement mondial dédié aux services financiers, organisé par...